Savings accountsGone are the days of 10% interest rates on your savings accounts. Most nowadays are lucky to give you more than 1% if you need to get access to your money quickly

This highlights the first thought you need to process before looking, how quickly will you need to access your money? If you need instant access most banks are offering 1% on a savings account , quite often these are limited to how much you can deposit and how often. Some operate on a monthly deposit mechanism. See the information below for more information |

|

One thing to remember, from April 2016 we will no longer be paying tax on the first £1000 interest earnt. This means for the majority of the U.K. Public that every £1 interest earn we are 20p better off.

Instant access accountsExactly as per the title, these accounts operate online or from a branch, they are ideal if you are wanting to save smaller amounts of money for something like a car. These are the lowest paying interest bracket, but mean you can get all your money when you need it (subject your banks daily withdrawal limits)

|

Fixed access accountsThese type of accounts tend to work on a fixed notice period before you can make a withdrawal. You will need to visit a branch or give the financial institute a call to arrange a date or withdrawal. These types of account are great if you are planning on savings for say a house deposit and don't want the money for a longer time.

|

Bonds

These Type of accounts Bring the best rates of savings interest. Your money is locked in for a fixed amount of time, usually 1,3 or 5 years. Once that time is up you will be offered the chance to withdraw the funds or re invest.

|

ISA

These are one of the best savings account for general all round use.

They don't offer the best interest rates but you don't pay tax on the interest and you can normally have the account as an online account or in branch |

Compound interest.

One thing I've tried explaining to my friend is compound interest. This is basically when you earn interest on your interest each month so your initial investment grows.

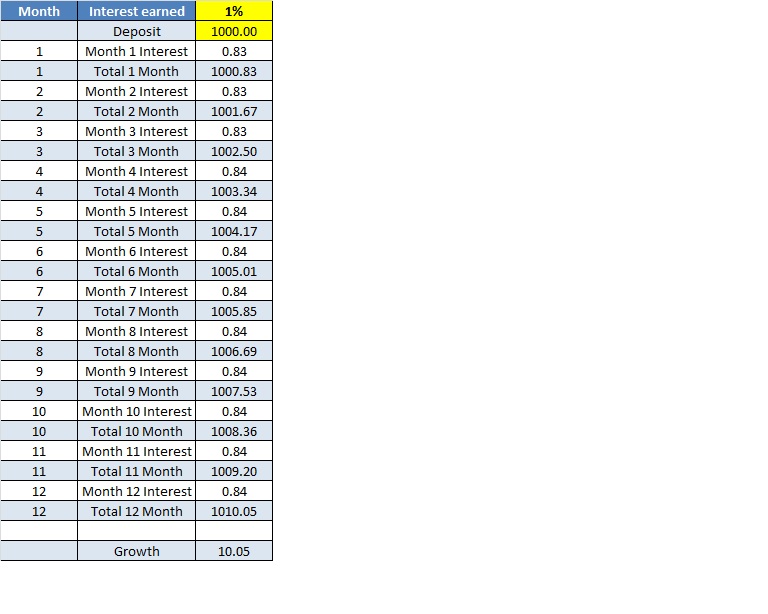

On a small interest paying account this can be quite slow , you can see on the table below if you started with £1000 in a 1% per year interest account you'd only have £1010.05 afters year £10.05 isn't much interest but you can see from the table how the interest increases each month

The workable Excel file on the attachment below the table can be manipulated to give an illustration of how interest grows depending on % interest and initial investment and how compound interest can work. This is much more applicable on mortgages or credit cards where hi balances or interest are used .

On a small interest paying account this can be quite slow , you can see on the table below if you started with £1000 in a 1% per year interest account you'd only have £1010.05 afters year £10.05 isn't much interest but you can see from the table how the interest increases each month

The workable Excel file on the attachment below the table can be manipulated to give an illustration of how interest grows depending on % interest and initial investment and how compound interest can work. This is much more applicable on mortgages or credit cards where hi balances or interest are used .

| compound_interest.xlsx |